RHI Tariff Degression for biomass boilers – Commercial RHI

The Government has adopted a mechanism for budget management of RHI payments which involves "degression" of tariff rates for technologies that are absorbing more cash from the RHI budget than Government had envisaged.

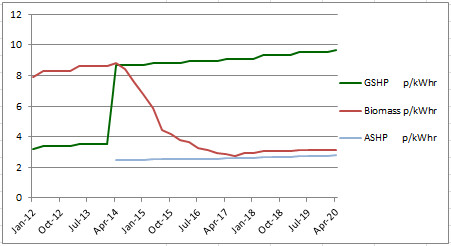

The first degression was a 5% reduction in the tariff for medium biomass from 1 July 2013.

The second degression was a 5% reduction in the tariff for small biomass from 1 July 2014 from 8.8 to 8.4p.

The third degression was a 10% reduction in the tariff for small biomass from 1 October 2014 to 7.6p.

The fourth degression was a further 10% reduction in the small biomass tariff from 1 January 2015 to 6.8p.

The fifth degression was a 15% reduction in the small biomass tariff from 1 April 2015 to 5.87p.

The sixth degression was a 25% reduction in the small biomass tariff from 1 July 2015 to 4.40p.

The seventh degression was a 5% reduction in the small biomass tariff from 1 October 2015 to 4.18p.

The eighth degression was a 10% reduction in the small biomass tariff from 1 January 2016 to 3.76p.

The ninth degression was a 5% reduction in the small biomass tariff from 1 April 2016 to 3.62p.

The tenth degression was a 10% reduction in the small biomass tariff from 1 July 2016 to 3.26p.

The eleventh degression was a 5% reduction in the small biomass tariff from 1 Oct to 3.10p.

The twelfth degression was a 5% reduction in the small biomass tariff from 1 Jan 17 to 2.95p.

The thirteenth degression was a 5% reduction in the biomass tariff from 1 April 17 to 2.85p.

The fourteenth degression is a 5% reduction in the biomass tariff from 1 July 17 to 2.71p.

Risk of further RHI Tariff Degression for biomass boilers

Because the take up of biomass boilers has been ahead of expectations there is a risk of further "degressions" to biomass tariffs.

RHI Tariff increases for ground source heat pumps

The uptake of GSHPs and solar thermal panels is only a small fraction of what DECC had anticipated. [The uptake of ground source heat pumps was initially depressed by the very attractive tariffs for PV and other renewable technologies offered by DECC from 2010 until Ofgem started to pay increased rates for GSHPs in June 2014. The rates for PV and biomass have since fallen sharply.]

The Commercial RHI tariff for ground source heat pumps more than doubled in 2014 and, from July 2015, the GSHP rate was twice the rate for small biomass. From 1 January 2017 it was three times the biomass rate.

The financial attractions of installing GSHPs has doubled at the same time as the other advantages of GSHPs are becoming more apparent:

- GSHPs emit no CO2 on site, and decreasing CO2 as electric power stations are being decarbonised

- GSHPs, once installed, require less work than biomass (no fuel deliveries, no ash, minimum servicing)

- GSHP installations last much longer than biomass installations (ground loops last over 50 years)

- GSHPs can provide cooling in summer as well as heating in winter

- installation of GSHPs, an invisible technology, requires no planning permission.

See Ground Source Heating See Ground Source Cooling See Ground Source Energy

RHI Tariff Tables

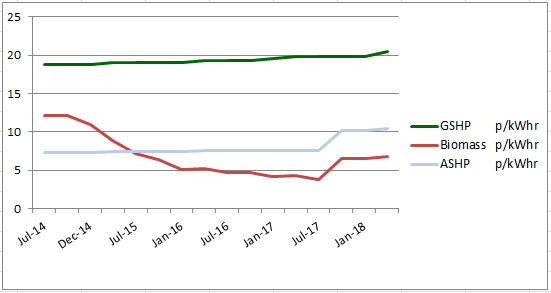

A summary of the current RHI rates is shown in the RHI Tariff Tables.

A summary of the RHI rates history is shown in the RHI Tariff Tables History.

RHI Biomass Tariff Degression – Domestic RHI

The Domestic RHI scheme started on 9 April 2014. The uptake of biomass greatly exceeded DECC's expectations and consequently the first degression of the domestic biomass tariff took place for applications received after 1 January 2015.

The first degression was a 10% reduction in the tariff from 12.2p to 10.98 on 1 January 2015.

The second degression was a 20% reduction to 8.93p in April.

The third degression was a 20% reduction to 7.14 in July

The fourth degression was a further 10% reduction to 6.43 from October.

The fifth degression was a 20% reduction to 5.14 from January 2016.

The sixth degression was a 20% reduction to 4.68 from July 2016.

The seventh degression was a 10% reduction to 4.21 from Jan 2017.

The eighth degression is a 10% reduction to 3.85 from July 2017.

See also: Banking on IHT The Merton Rule Economic Renewable Energy